I’ve just released a new PFF white paper looking at the hysteria that has often accompanied major media mergers and then taking a look at the marketplace reality years after the fact. Here‘s the PDF, but I have also pasted the entire thing down below.

_____________________________

A Brief History of Media Merger Hysteria:

From AOL-Time Warner to Comcast-NBC

by Adam Thierer

Although the pending union of Comcast and NBC Universal has not yet made it to the altar, Chicken Little-esque wails about the marriage have already begun in earnest. For example, the pro-regulatory media organization Free Press has already set up a website to complain about the deal.[1] And Jeff Chester, executive director of the Center for Digital Democracy, has called it “an unholy marriage.”[2] The fever only promises to spread once the deal is formally announced, and a lengthy fight over the deal is expected at the Federal Communications Commission (FCC) and whichever antitrust agency reviews the deal.[3]

But reality tends to play out somewhat less dramatically than the script penned by the media worrywarts. It’s worth looking back at some of the more prominent examples of media merger hysteria in recent years to understand why such panic is unwarranted, and why a deal between Comcast and NBC Universal is unlikely to lead to the sort of problems that the pessimists suggest.[4]

AOL-Time Warner: From the “New Totalitarianism” to Digital Divorce Court in Less Than a Decade

When the mega-merger between media giant Time Warner and Internet superstar AOL was announced in early 2000, the marriage was greeted with a cacophony of righteous indignation and apocalyptic predictions. When referring to the dangers of the deal, syndicated columnist Norman Solomon, a longtime associate of the media watch group Fairness & Accuracy In Reporting, summoned the ghost of Aldous Huxley when he and referred to the transaction in terms of “servitude,” “ministries of propaganda,” and “new totalitarianisms.”[5] Similarly, USC Professor of Communications Robert Scheer wondered if the merger represented “Big Brother” and claimed, “Diversity is out, niches are gone, it’s Skippy peanut butter time. AOL is the Levitown of the Internet, mom and apple pie, ‘50s boredom, conformity and dullness as a virtue: A Net nanny reigning in potentially restless souls.”[6]

Such pessimistic predictions proved wildly overblown. To say that the merger failed to create the sort of synergies (and profits) that were originally hoped for would be an epic understatement.[7] The titles of two popular books about the deal summed up the firm’s troubles: One was entitled Fools Rush In (by Nina Munk) and the other, There Must Be a Pony in Here Somewhere (by Kara Swisher and Lisa Dickey).[8]

The numbers were mind-boggling. By April 2002, just two years after the deal was struck, AOL-Time Warner had already reported a staggering $54 billion loss.[9] By January 2003, losses had grown to $99 billion.[10] By September 2003, Time Warner decided to drop AOL from its name altogether and the deal continued to slowly unravel from there.[11] In a 2006 interview with the Wall Street Journal, Time Warner President Jeffrey Bewkes famously declared the death of “synergy” and went so far as to call synergy “bullsh*t”![12] In early 2008, Time Warner decided to shed AOL’s dial-up service[13] and now is set to spin off AOL entirely.[14] Looking back at the deal, Fortune magazine senior editor at large Allan Sloan called it the “turkey of the decade”:

The day the deal was announced, Jan. 10, 2000, Time Warner closed at the equivalent of $184.50 a share. After almost 10 years of travail, the $184.50 has shrunk to about $42.25, consisting of one Time Warner share and a quarter of a Time Warner Cable share. The 77 percent decline is triple the decline in the Standard & Poor’s 500-stock index over the same period.[15]

And the Time Warner-AOL split wasn’t the end of this messy divorce process. In 2008, Time Warner Cable and Time Warner Entertainment decided to split.[16] Time Warner has even spun off some of its oldest properties. In 2006, it announced that it was putting 18 of the 50 magazines in its Time magazine division up for sale.[17]

As is always the case, these divestitures and down-sizing efforts garnered little attention compared with the hullaballoo and hysteria that accompanied the announcement of the deal back in 2000.[18]

News Corp/DirecTV: Murdoch’s “Digital Death Star” Blows Up

No media industry personality attracts more attention (or angst) than News Corp. Chairman and CEO Rupert Murdoch. The popular leftist blog The Daily Kos has likened him to “a fascist Hitler antichrist.”[19] And CNN founder Ted Turner once compared the popularity of the News Corp.’s Fox News Channel to the rise of Adolf Hitler prior to World War II.[20] Alternatively, Murdoch has been accused of being a Marxist.[21] Meanwhile, Karl Frisch, a Senior Fellow at Media Matters for America, speaks of Murdoch’s “evil empire”[22] and a recent MSNBC poll has asked people to vote on the question: “Is Rupert Murdoch evil?”[23] In 2003, when asked by talk show host Chris Matthews, “Would you break up [News Corp.-owned] Fox?” then Democratic presidential candidate Howard Dean answered, “On ideological grounds, absolutely yes.”[24] And in their book Our Media, Not Theirs, John Nichols and Robert McChesney took the Murdoch-as-evil-overlord storyline to its logical extreme when they suggested Hollywood was on to something by scripting a media tycoon like Murdoch as the bad guy in a James Bond movie: “No wonder conspiracy theories are so popular in America; no wonder, when the makers of James Bond movies look for believable villains these days, they eschew Eurotrash bad guys for more credibly threatening villains such as the Rupert Murdoch-like media baron of 1997’s Tomorrow Never Dies.”[25]

These Murdochian fears came to a head in 2003 when News Corp. announced it was pursuing a takeover of satellite television operator DirecTV. Paranoid predictions of a pending media apocalypse followed. A group of regulatory activists filed joint comments to the FCC claiming that if News Corp. and DirecTV were allowed to merge, “the result will be unprecedented concentration within all aspects of the television marketplace, as well as increased prices for consumers of cable and satellite television.”[26] Similarly, then-FCC Commissioner Jonathan Adelstein worried that the deal would “result in unprecedented control over local and national media properties in one global media empire. Its shockwaves will undoubtedly recast our entire media landscape.” He continued; “With this unprecedented combination, News Corp. could be in a position to raise programming prices for consumers, harm competition in video programming and distribution markets nationwide, and decrease the diversity of media voices.”[27]

Not to be outdone, full-time media fussbudget Jeff Chester predicted that Murdoch would use this “Digital Death Star” as the base of a nefarious scheme to conquer the media universe:

Murdoch will use DirecTV as a ‘death star’ to force his programming on cable companies by threatening a price war unless they give Fox favorable access. Since News Corp will control cable TV’s principal multichannel competitor, it will easily create new channels—unlike anyone else in the TV business. Rather than engage in open combat and competition, cable powerbrokers such as Comcast and AOL-Time Warner will likely accommodate Murdoch and add his new channels to their own services. Imagine Fox News on steroids. Worse, with DirecTV’s capacity to ‘spotbeam’ channels to serve distinct communities, localized versions of Fox programs could be available in major cities across the nation.[28]

Imagine the horror of new, “spotbeamed” local media competition! However, unlike the destruction of the planet Alderaan by the Death Star in Star Wars,[29] no one was harmed in the making of the News Corp-DirecTV marriage. Indeed, the rebels would get the best of Darth Murdoch since his “Digital Death Star” was abandoned just three years after construction. In December 2006, News Corp. decided to divest the company to Liberty Media Corporation in an effort to win back more controlling News Corp. stock.[30]

Ironically, many of the same groups that had vociferously protested the original News Corp-DirecTV deal again found reason to complain when the deal was being undone! The FCC’s failure to implement various restrictions as part of the license transfer, they claimed, would “result in continuing control by News Corp. over content distribution, harming competition in both the programming and distribution markets, reducing consumer choice and raising cable prices.”[31] Unsurprisingly, little mention was made of the previous round of pessimistic predictions or whether there had ever been any merit to the lugubrious lamentations of the media critics.

Sirius-XM: “Merger to Monopoly” or Prelude to Bankruptcy?

Some of the most entertaining and wrong-headed predictions about the future of the media marketplace often come from media moguls themselves. For example, back in 2003, when he was still President and Chief Operating Officer of Viacom, Mel Karmazin said in reference to Microsoft, AOL Time Warner, and Comcast: “I can’t imagine being a competitor with any of these guys.”[32] Just six years later, however, plenty of others are competing with those companies. Microsoft finds itself in a heated war with Google on all fronts, AOL-Time Warner has fallen apart, and Comcast is squaring off against telco (e.g., Verizon’s FiOS and AT&T U-Verse) and online video competitors (e.g., YouTube, Hulu) that were unfathomable in 2003—not to mention the traditional satellite TV competitors they still face. Meanwhile, Karmazin abandoned Viacom and is now struggling to find a way to make subscription-based satellite radio survive the ongoing digital music bloodbath caused by the rise of online music services and a little thing called the iPod.

Of course, hysteria ran rampant when Sirius and XM were merging, too. Critics called it a “merger to monopoly” and predicted a variety of coming calamities.[33] National Association of Broadcasters Vice President Dennis Wharton described the merger as a “monopoly platform for offensive programming” that would be “anti-consumer.”[34] Mr. Wharton later remarked that the merged firms “will raise prices, won’t improve their technology and will limit their offerings.”[35] A coalition of six non-profits claimed that the merger was “perhaps the worst offense against the basic principle that competition is the consumer’s best friend” and, if approved, “a tsunami of mergers could ripple through the digital space at the worst possible moment.”[36] They predicted that “once the competition is eliminated, prices will rise over time,” “innovation will slow to the pace preferred by the monopolist and consumers will be much worse off in the long run.”[37] Another coalition argued that the new company would “abuse consumers, artists and other input suppliers in the satellite radio market.”[38]

In the end, the merger took an astonishing 500-plus days for the FCC to finally approve[39] and was conditioned with a lengthy set of “voluntary concessions” to supposedly rectify these potential harms—including pricing constraints that could limit the firm’s ability to cover costs and pay down debt over time.

Unsurprisingly, things haven’t turned out so well for Sirius XM. When the merger was finally approved by the FCC in August 2008, Commissioner Copps dissented vigorously on various grounds but specifically insisted that, “We must assume that the marketplace can support two financially viable competitors.”[40] Unfortunately for Commissioner Copps—as well as Sirius XM—it’s not even clear that the market can sustain one satellite radio provider. The company’s stock went into freefall following completion of the deal and, at one point, its stock fell below 10 cents per share. The company flirted with bankruptcy in February of this year as “satellite radio failed to win over many younger listeners, and competition from other sources slowed subscriber growth.”[41] In March 2009, Karmazin orchestrated a cash-for-stock swap with Liberty Media to get a $530 million lifeline and avoid bankruptcy.[42] But even with the cash infusion Sirius XM faces an uncertain future with stiff competition.[43] “Sirius is girding for slower growth than in the past,” notes Olga Kharif of Business Week, “and analysts remain concerned about the company’s ability to control costs.”[44] Former stockbroker and RealMoney.com contributor Tim Melvin predicts the overleveraged company “will disappear from the landscape. The subscribers will go to another tech or entertainment company in bankruptcy proceedings. Subscription radio just does not have that much appeal to most people.”[45]

Whether Melvin’s dour forecast for satellite radio proves accurate remains to be seen. What’s clear, however, is that the fears bandied about by critics when the Sirius-XM deal was pending have not come to pass.

Murdoch’s Wall Street Journal Quest

In 2007, Rupert Murdoch announced his desire to purchase The Wall Street Journal. Once again, a great deal of hand-wringing ensued. “This takeover is bad news for anyone who cares about quality journalism and a healthy democracy,” argued Robert McChesney. “Giving any single company—let alone one controlled by Rupert Murdoch—this much media power is unconscionable.”[46] And FCC Commissioner Copps warned that “It will create a single company with enormous influence over politics, art and culture across the nation and especially in the New York metropolitan area.”[47]

Today, however, the Journal keeps humming along and continues to produce some of the finest journalism on the planet. Meanwhile, “politics, art and culture” seem largely unaffected by the deal—either in New York or the nation.

And the deal certainly hasn’t made Murdoch or News Corp. any richer. “His purchase of The Wall Street Journal is widely seen as one of the worst moves of his career,” notes Michael Wolff of Vanity Fair.[48] News Corp. has already taken a whopping $3 billion write-down on the deal. Considering the $5 billion price tag Murdoch paid two years ago, one wonders if he’ll hold on to this property any longer than he did DirecTV.

Comcast-NBC Universal: Debunking the Fears Preemptively

No doubt we’ll soon be hearing many of these same apocalyptic predictions about the Comcast-NBC deal. Free Press has said the new entity “will have an incentive to prioritize NBC shows over other local and independent voices and programs, making it even harder to find alternatives on the cable dial.”[49] And Free Press Executive Director Josh Silver has called for the Obama Administration to block the deal saying “it would further starve Americans of [media] diversity.”[50] Even competitors are complaining. Liberty Media Corp. Chairman John Malone, which owns DirecTV, has suggested that they might push the government to reject the deal.[51] Many other rivals will likely join that bandwagon.

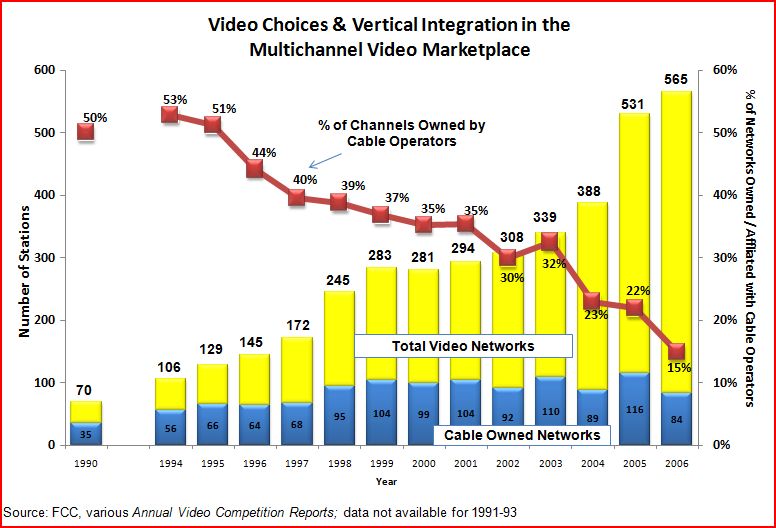

These critics will likely raise vertical integration fears and claim that Comcast will act as a “gatekeeper” by limiting the ability of independent voices to get a slot on cable distribution systems, or by withholding NBC-Universal content from other platforms and providers. But there’s little historical evidence that suggests this will be a problem. As the adjoining exhibit illustrates, the overall number of video programming channels available in America has skyrocketed, from just 70 channels in 1990 to 565 channels in 2006, the last year for which the FCC has made data available.

More importantly—and despite claims to the contrary—vertical integration in the video marketplace has plummeted over the past two decades. While many more cable and satellite networks are available today than ever before, the greatest share of the growth in the multichannel video marketplace has come from independently owned video networks. Since 1990, the number of cable-owned or affiliated channels has increased slightly, but it pales in comparison with the growth of independently owned and operated video networks. In real terms, therefore, the percentage of the overall video marketplace controlled (i.e., owned and operated) by cable companies has plummeted—from 50% in 1990 to just 14.9% in 2006. Moreover, in the wake of the Time Warner Cable and Time Warner Entertainment divorce, vertical integration in the cable sector has probably fallen into the single digits. Even if the merger of Comcast and NBC-Universal results in slight increase in industry vertical integration, it almost certainly will not surpass 20 percent. Consequently, as far as vertically integrated industries go, it is impossible to conclude that this market could be characterized as being controlled by “gatekeepers.”

It is difficult to imagine that Comcast would buck these trends and begin restricting independent options on its systems or withhold its content from others. Video distributors don’t make money by restricting choice. Consumers would flock to alternative video providers and media services if Comcast played such games. The great thing about the modern media marketplace is that there is always another place for consumers to turn to find something they want.[52] Sports programming could be an exception to the rule, and is the one issue that Comcast may need to bargain over with FCC regulators or antitrust officials since they own regional sports networks that other video distributors want access to.[53] But traditional concerns about access to over-the-air broadcast signals (namely, the NBC local broadcast television properties) shouldn’t be as much of an issue today as it was the past. Frankly, local broadcasters need all the eyeballs they can get these days. Thus, it’s unlikely that Comcast would try to withhold those stations from other video distributors, especially since a great deal of NBC programming is already available through other means. And intense competition exists for some of the most important news and informational services that NBC offers, such as local news, weather, and traffic.

Overall, therefore, it’s hard to see the case for the FCC rejecting the deal. Regulators need to be forward-looking about what is driving this deal. This deal isn’t about protecting old markets but instead about building new ones. “The real motivation behind this deal,” argues Mike Berkley, former CEO of SplashCast Media, “is survival.”

Comcast understands that the price point for distributing TV into homes is going to fall dramatically in the coming years. Comcast’s 3 distribution products, Voice – TV – Internet, are collapsing into just one, single product: Internet. This poses a huge threat to Comcast’s top line. As such, Comcast is hedging through diversification into content, moving up the media value chain. Comcast will be looking to replace lost revenue in distribution with revenue from content (advertising, subscriptions, etc).[54]

Similarly, Wall Street Journal business columnist Holman Jenkins points out that Comcast is scrambling to find a way to rework their business model as the era of set-top box-delivered video slowly gives way to a world of ubiquitously available online video:

This would be a merger, after all, of two businesses that seem headed toward some combination of the fates of newspapers, music CDs and the old wireline telephone business. Customers want the product for free. Comcast’s lifeblood, the $100-a-month cable bill and the $50-a-month broadband bill, increasingly look like duplicative expenses. And so on.

True, the number of households that have actually dropped their cable subscriptions in favor of subsisting on TV streamed or downloaded from the Internet is not yet large. But for the Roberts family and its Comcast property, their worst fears lurk just around the corner—being reduced to a “dumb pipe,” subject to commodity pricing while somebody else (Google) makes all the money.

Yet an escape route is vexingly hard to envision. Time Warner and Comcast have been talking up plans to make their respective cable lineups available by computer—as long as you keep paying your cable bill. This is a stopgap, especially appealing to anyone who owns two homes but wants to pay only one cable bill. Never mind, too, that hundreds of shows are already available online for free, via Web sites operated by none other than Comcast and the TV networks themselves.[55]

In light of such technological upheaval and marketplace uncertainty, it’s important that regulators proceed cautiously when reviewing this deal or future deals.

Conclusion: Let Markets Evolve

The point here is not that media mergers are inherently good or always make sense. Indeed, as the examples discussed above illustrate, mergers sometimes prove to be huge blunders.[56] But the hysteria sometimes heard before media mergers are consummated rarely bears any relationship to reality once the deals move forward. Media markets are extremely dynamic and prone to disruptive change and technological leap-frogging. Mergers are often one response to that turbulence.

But mergers are no panacea, and they often fail to produce the “synergies” hoped for. A 2004 survey by McKinsey & Co. found that “Nearly 70 percent of the mergers in our database failed to achieve the revenue synergies estimated by the acquirer’s management.”[57] Perhaps, therefore, the best argument for blocking media mergers is not their potentially pernicious effect on markets or consumers, but rather to save the merging firms (and their stockholders) from a miserable marriage!

On the other hand, experimenting with alternative business models and ownership structures is an important part of any dynamic market, because markets are not static but represent and ongoing processes of entrepreneurial “discovery.”[58] Thus, policymakers would be wise to avoid micro-managing mergers and instead let things run their course. Sometimes collaboration makes a great deal of sense, especially when the significant costs of providing a media service becomes impossible absent a partnership. Indeed, federal officials and agencies are currently exploring how (or whether) journalism can survive an era of seeming perpetual media upheaval.[59] Healthy media companies certainly must be part of the answer and new ownership arrangements might be part of the solution.

Given how difficult it is to predict the future course of events in this chaotic sector, humility—not hubris—is the sensible disposition when it comes to media merger policy. At a minimum, policymakers should insist that ongoing debates are governed by facts instead of fanaticism, because, if the past decade is any guide, discussions about media mergers have been more often rooted in hyperbolic rhetoric and unsubstantiated hysteria.

[2] Quoted in Cecilia Kang, Public Interest Groups Rail against a Comcast and NBC Merger, Washington Post, Post Tech Blog, Nov. 9, 2009, http://voices.washingtonpost.com/posttech/2009/11/for_example_were_advancing_tv.html

[3] “For regulators, a deal like this is a gift; an occasion to impose their will upon needy companies that would otherwise be outside their regulatory reach.” Craig Moffett, Bernstein Research, Comcast: Snatching Defeat from the Jaws of Victory? Oct. 23, 2009, at 14.

[4] Cecilia Kang, A New Kind of Company, A New Kind of Challenge for Feds, Washington Post, Nov. 26, 2009, at 1, www.washingtonpost.com/wp-dyn/content/article/2009/11/26/AR2009112602500.html

[5] Norman Soloman, AOL Time Warner: Calling The Faithful To Their Knees, Jan. 2000, www.fair.org/media-beat/000113.html

[6] Robert Scheer, Confessions of an E-Columnist, Jan. 14, 2000, Online Journalism Review, www.ojr.org/ojr/workplace/1017966109.php

[7] Looking back at the deal almost ten years later, AOL co-founder Steve Case said, “The synergy we hoped to have, the combination of two members of digital media, didn’t happen as we had planned.” Quoted in Thomas Heath, The Rising Titans of ’98: Where Are They Now?, Washington Post, Nov. 30, 2009, www.washingtonpost.com/wp-dyn/content/article/2009/11/29/AR2009112902385.html?sub=AR

[8] Nina Munk, Fools Rush In: Steve Case, Jerry Levin, and the Unmaking of AOL Time Warner (New York: Harper Business, 2004); Kara Swisher and Lisa Dickey, There Must Be a Pony in Here Somewhere: The AOL Time Warner Debacle and the Quest for a Digital Future (New York: Crown Business, 2003).

[9] Frank Pellegrini, What AOL Time Warner’s $54 Billion Loss Means, April 25, 2002, Time Online, www.time.com/time/business/article/0,8599,233436,00.html

[10] Jim Hu, AOL Loses Ted Turner and $99 billion, CNet News.com, Jan. 30, 2004, http://news.cnet.com/AOL-loses-Ted-Turner-and-99-billion/2100-1023_3-982648.html

[11] Jim Hu, AOL Time Warner Drops AOL from Name, CNet News.com, Sept. 18, 2003, http://news.cnet.com/AOL-Time-Warner-drops-AOL-from-name/2100-1025_3-5078688.html

[12] Matthew Karnitschnig, After Years of Pushing Synergy, Time Warner Inc. Says Enough, Wall Street Journal, June 2, 2006, http://online.wsj.com/article/SB114921801650969574.html

[13] Geraldine Fabrikant, Time Warner Plans to Split Off AOL’s Dial-Up Service, New York Times, Feb. 7, 2008, www.nytimes.com/2008/02/07/business/07warner.html?_r=1&adxnnl=1&oref=slogin&adxnnlx=1209654030-ZpEGB/n3jS5TGHX63DONHg

[14] John Letzing, AOL, On The Verge Of Independence, Weighs On Parent, Wall Street Journal, Nov. 4, 2009, http://online.wsj.com/article/BT-CO-20091104-718782.html

[15] Allan Sloan, ‘Cash for . . .’ and the Year’s Other Clunkers, Washington Post, Nov. 17, 2009, www.washingtonpost.com/wp-dyn/content/article/2009/11/16/AR2009111603775.html

[16] Tim Arango, Time Warner Spinning Off Cable Unit, New York Times, April 30, 2008, www.nytimes.com/2008/04/30/business/30warner-web.html?ref=technology

[17] Carolyn Pritchard, Time Inc. to Sell 18 Magazine Titles, MarketWatch, Sept. 12, 2006, www.marketwatch.com/News/Story/Story.aspx?guid=%7B94967C37%2D9B4A%2D4C1A%2D8AC0%2D64904C1267A1%7D&dist=rss&siteid=mktw&rss=1

[18] “Break-ups and divestitures do not generally get front-page treatment,” notes Ben Compaine, author of Who Owns the Media? See Ben Compaine, Domination Fantasies, Reason, Jan. 2004, p. 28, www.reason.com/news/show/29001.html

[19] www.dailykos.com/story/2009/9/7/778254/-Rupert-Murdoch-is-a-Fascist-Hitler-Antichrist

[20] Jim Finkle, Turner Compares Fox’s Popularity to Hitler, Broadcasting & Cable, Jan. 25, 2005, www.broadcastingcable.com/CA499014.html

[21] Ian Douglas, Rupert Murdoch is a Marxist, Telegraph.Co.UK, Nov. 9, 2009, http://blogs.telegraph.co.uk/technology/iandouglas/100004169/rupert-murdoch-is-a-marxist

[22] Karl Frisch, Fox Nation: The Seedy Underbelly of Rupert Murdoch’s Evil Empire? MediaMatters.org, June 2, 2009, http://mediamatters.org/columns/200906020036

[23] www.msnbc.msn.com/id/19817142/

[24] Dean Vows to ‘Break Up Giant Media Enterprises,’ The Drudge Report, Dec. 2, 2003, www.drudgereport.com/dean1.htm; Bill McConnell, Dean Threatens to Break Up Media Giants, Broadcasting & Cable, Dec. 3, 2003, www.broadcastingcable.com/index.asp?layout=articlePrint&articleID=CA339546.

[25] John Nichols and Robert W. McChesney, Our Media, Not Theirs: The Democratic Struggle against Corporate Media (New York: Seven Stories Press, 2002) at 31.

[26] Consumers Union, Consumer Federation of America, Center for Digital Democracy, and Media Access Project, Comments In the Matter of News Corporation/Fox Entertainment Group Merger with Hughes Electronics Corporation/DirecTV, MB Docket No. 03-124, July 1, 2003, www.consumersunion.org/pdf/0701-DirecTV.pdf

[27] Dissenting Statement of Commissioner Jonathan S. Adelstein, Re: General Motors Corporation and Hughes Electronics Corporation, Transferors, and The News Corporation Limited, Transferee, MB Docket No. 03-124, Jan. 14, 2004, http://hraunfoss.fcc.gov/edocs_public/attachmatch/FCC-03-330A6.doc

[28] Jeff Chester, Rupert Murdoch’s Digital Death Star, AlterNet, May 20, 2003, www.alternet.org/story/15949

[29] Destruction of Alderaan, Wookieepedia: The Star Wars Wiki, http://starwars.wikia.com/wiki/Destruction_of_Alderaan

[30] News Corporation and Liberty Media Corporation Sign Share Exchange Agreement, News Corp Press Release, Dec. 22, 2006, www.newscorp.com/news/news_322.html. A frustrated Murdoch referred to DirecTV as a “turd bird” just before he sold it off. See Jill Goldsmith, Murdoch Looks to Release Bird, Variety, Sept. 14, 2006, www.variety.com/article/VR1117950090.html?categoryid=1236&cs=1

[31] Consumers Union, Consumer Federation of America, Free Press, and Media Access Project, Comments In the Matter of Authority to Transfer Control of DirecTV, MB Docket No. 07-18, March 23, 2007, www.mediaaccess.org/file_download/177

[32] Richard Linnett, Media Rivals Backslap at Cable Conference, AdAge.com, June 10, 2003.

[33] Dissenting Statement of Commissioner Michael J. Copps, Applications for Consent to the Transfer of Control of Licenses, XM Satellite Radio Holdings Inc., Transferor, to Sirius Satellite Radio Inc., Transferee, MB Docket No. 07-57, Aug. 5, 2008, http://hraunfoss.fcc.gov/edocs_public/attachmatch/FCC-08-178A3.pdf

[34] Dennis Wharton, National Association of Broadcasters, NAB Statement in Response to Sirius/XM Proposed Merger, Feb. 19, 2007, www.nab.org/AM/Template.cfm?Section=Search&template=/CM/HTMLDisplay.cfm&ContentID=8258.

[35] Peter Whoriskey and Kim Hart, Justice Dept. Approves XM-Sirius Radio Merger, The Washington Post, Mar. 25, 2008, www.washingtonpost.com/wp-dyn/content/article/2008/03/24/AR2008032401645.html.

[36] The XM-Sirius Merger: Monopoly or Competition from New Technologies: Hearing Before the Senate Committee on the Judiciary Subcommittee on Antitrust, Competition Policy and Consumer Rights, 3 & 6 (March 20, 2007) (statement of Common Cause et. al), www.hearusnow.org/fileadmin/sitecontent/2007_-_0320_Public_Interest_Groups_Statement_-_Senate_Judiciary.pdf

[37] Id. at 6.

[38] Common Cause, Consumer Federation of America, Consumers Union, Free Press, Comments in the Matter of Consolidated Application for Authority To Transfer Control of XM Radio Inc. and Sirius Satellite Radio Inc., MB Docket No. 07-57July 9, 2007, at 1, www.hearusnow.org/fileadmin/sitecontent/xm-sirius_comments.pdf

[39] James Gattuso, Day 505: The XM-Sirius Circus Is Finally Over, Technology Liberation Front Blog, Aug. 7, 2008, http://techliberation.com/2008/08/07/day-505-the-xm-sirius-circus-is-finally-over

[40] Dissenting Statement of Commissioner Michael J. Copps, Applications for Consent to the Transfer of Control of Licenses, XM Satellite Radio Holdings Inc., Transferor, to Sirius Satellite Radio Inc., Transferee, MB Docket No. 07-57, Aug. 5, 2008, http://hraunfoss.fcc.gov/edocs_public/attachmatch/FCC-08-178A3.pdf

[41] Andrew Ross Sorkin & Zachery Kouwe, Sirius XM Prepares for Possible Bankruptcy, New York Times, Feb. 10, 2009, www.nytimes.com/2009/02/11/technology/companies/11radio.html

[42] Jon Birger, Mel Karmazin Fights to Rescue Sirius, Fortune.com, March 16, 2009, http://money.cnn.com/2009/03/13/technology/birger_sirius.fortune/index.htm

[43] Former stockbroker and RealMoney.com contributor Tim Melvin worries about the “significant competition for the company going forward” He notes:

Most of the younger people I know have iPod docks in their vehicles for listening to music. Smartphones are bringing music and podcasts to mobile consumers. E-reading machines have wireless connections that can eventually deliver content on a subscription or pay-per-use basis. I really do not need the sports channels from Sirius if I can watch and listen to the games I want on my phone. As time goes by, satellite radio will be viewed as a stepping-stone technology that was replaced by smartphones and other portable media devices.

Tim Melvin, Sirius’ Hopes Keep Slipping Away, The Street.com, Nov. 10, 2009, www.thestreet.com/story/10624757/1/sirius-hopes-keep-slipping-away.html?cm_ven=GOOGLEFI

[44] Olga Kharif, Sirius XM: The Good and Bad Earnings News, Business Week, Nov. 5, 2009, www.businessweek.com/technology/content/nov2009/tc2009115_002716.htm

[45] Melvin, supra 39.

[46] Robert McChesney, Murdoch’s Deal for the Journal: Yet Another Blow for Journalism, Free Press Press Release, July 30, 2007, www.freepress.net/release/260

[47] Michael Copps, Letter to FCC Chairman Kevin Martin, Oct. 25, 2007, http://hraunfoss.fcc.gov/edocs_public/attachmatch/DOC-277576A1.pdf

[48] Michael Wolff, Rupert to Internet: It’s War! Vanity Fair, Nov. 2009, at 112.

[49] www.freepress.net/comcast

[50] Josh Silver, Too Big to Block? Why Obama Must Stop the Comcast-NBC Merger, Huffington Post, Nov. 13, 2009, www.huffingtonpost.com/josh-silver/too-big-to-block-why-obam_b_356826.html

[51] www.forbes.com/feeds/afx/2009/11/19/afx7143505.html

[52] Adam Thierer and Grant Eskelsen, The Progress & Freedom Foundation, Media Metrics: The True State of the Modern Media Marketplace, Summer 2008, www.pff.org/mediametrics

[53] However, experience with regulation of sports programming suggests that FCC meddling has had negative unintended consequences. See W. Kenneth Ferree, Competition in the Sports Programming Marketplace, Testimony before the Subcommittee on Telecommunications and the Internet, House Committee on Energy and Commerce, March 5, 2008, www.pff.org/issues-pubs/testimony/2008/030508ferreetestimony.pdf; Barbara Esbin, Unable to Watch the Big Game? Testimony before the National Conference of State Legislatures Communications, Financial Services and Interstate Commerce Committee, Apr. 25, 2008, www.pff.org/issues-pubs/testimony/2008/080425esbinNCSLpresentation.pdf

[54] Mike Berkley, The Comcast-NBC Deal is a Defensive Move by Comcast. It’s about Survival, TV News Stream, Nov. 16, 2009, http://tvnewsstream.com/the-comcast-nbc-deal-is-a-defensive-move-by-c

[55] Holman Jenkins, The Economics of Jay Leno, Wall Street Journal, Nov. 18, 2009, at A17, http://online.wsj.com/article/SB10001424052748704431804574541684183772504.html

[56] Chris O’Brien, Beware the Hype Around Mergers, MercuryNews.com, Nov. 12, 2009, www.mercurynews.com/chris-obrien/ci_13756963?nclick_check=1

[57] Scott A. Christofferson, Robert S. McNish & Diane L. Sias, Where Mergers Go Wrong, McKinsey on Finance, Winter 2004, at 2, http://westportcapital.com/library/McKinsey_Where_Mergers_Go_Wrong.pdf. The authors noted that, “acquirers face an obvious challenge in coping with an acute lack of reliable information. They typically have little actual data about the target company, limited access to its managers, suppliers, channel partners, and customers, and insufficient experience to guide synergy estimation and benchmarks.”

[58] See, e.g., Israel M. Kirzner, Competition, Regulation, and the Market Process: An “Austrian” Perspective, Cato Institute Policy Analysis No. 18, 1982, www.cato.org/pubs/pas/pa018.html

[59] For example, congressional hearings have been held on this topic and the Federal Trade Commission is holding a workshop on December 1st and 2nd asking, “Will Journalism Survive the Internet Age?” www.ftc.gov/opp/workshops/news/index.shtml

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.