[Cross posted at Truthonthemarket]

Basic economic theory underlies the conventional antitrust wisdom that if a merger makes the merging party a more effective competitor by lowering its costs, rivals facing this more effective competitor post-merger are made worse off, but consumers benefit. On the other hand, if a merger is likely to result in collusion or a unilateral price increase, the rival firm is made better off while consumers suffer. In the latter case — the one the DOJ complaint asserts we are experiencing with respect to the proposed AT&T merger — marketwide coordination or reduction of competition resulting in higher prices makes the non-merging rival better off.

Basic economic theory thus generates a set of clear testable implications for the DOJ’s theory of the transaction:

- events that the merger more likely should have a negative impact upon non-merging rivals’ stock prices when the merger is procompetitive (reflecting the likelihood the firm will face a more efficient, lower-cost rival in the future);

- events that make a merger less likely should have a positive impact upon non-merging rivals’ stock prices when the merger is procompetitive (reflecting the reduced likelihood that the merger will face the more efficient competitor in the future)

- by similar economic logic, events that make an anticompetitive merger more likely to occur should result in increase non-merging rivals’ stock prices (who will benefit from higher market prices) while events that make an anticompetitive merger less likely should decrease non-merging rivals’ stock prices.

The DOJ complaint clearly stakes out its position that the merger will be anticompetitive, and result in higher market prices. Paragraph 36 of the DOJ’s complaint focuses upon potential post-merger coordination:

The substantial increase in concentration that would result from this merger, and the reduction in the number of nationwide providers from four to three, likely will lead to lessened competition due to an enhanced risk of anticompetitive coordination. … Any anti competitive coordination at a national level would result in higher nationwide prices (or other nationwide harm) by the remaining national providers, Verizon, Sprint, and the merged entity. Such harm would affect consumers all across the nation, including those in rural areas with limited T-Mobile presence.

Paragraph 37 of the DOJ complaint turns to unilateral effects:

The proposed merger likely would lessen competition through elimination of head-to-head competition between AT&T and T-Mobile. … The proposed merger would, therefore, likely eliminate important competition between AT&T and T-Mobile.

If the DOJ’s allegations are correct, one would expect the market price for prominent non-merging rivals such as Sprint to fall upon today’s announcement that the DOJ will challenge the merger. This is because the announcement decreases the likelihood that an anticompetitive merger will occur, and thus deprives the opportunity for non-merging rivals to enjoy the increased market prices and margins that would follow from post-merger collusion or unilateral price increases.

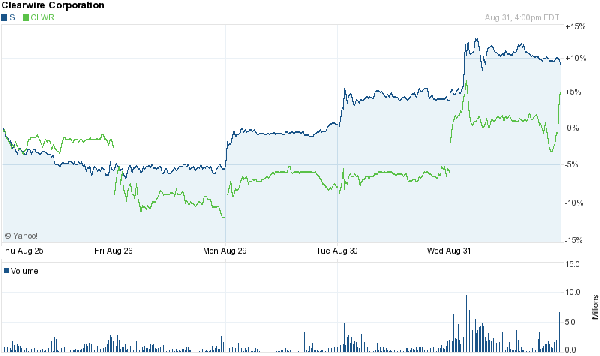

The NY Times Dealbook headline suggests otherwise: “Sprint Shares Surge on AT&T Setback.” Geoff highlighted several of the DOJ’s claims in the report. As the case unfolds, I think an important question to ask is how many of those allegations are consistent with the following data showing the market reactions of Sprint and Clearwire stock prices today. I’ve included Clearwire both because Sprint owns a majority share in it and because of its recent announcement of plans to enter the 4G LTE space.

I’ve not run a full-blown event study here, obviously. But the positive jump for Sprint (Blue Line) & Clearwire (Green Line) today in response to the announcement is hard to miss. How many of the statements in the DOJ complaint, press release and analysis are consistent with this market reaction? If the post-merger market would be less competitive than the status quo, as the DOJ complaint hypothesizes, why would the market reward Sprint and Clearwire for an increased likelihood of facing greater competition in the future? The simplest alternative hypothesis is that the merger is likely procompetitive and rivals are enjoying a premium for the increased likelihood that they will avoid more intense competition in the future. Is there a reason here to reject that simple hypothesis? Will the market reaction induce the DOJ to revisit its priors?

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.