“How many old media companies would you need to stack on top of one another to equal the value of Google?” That question was put to me last year by a reporter who was interviewing me for a story he was doing about the future of traditional media operators. I was explaining to him how many traditional media operators faced three ominous developments / threats that raised serious questions about their long-term viability: (1) Loss of consumer confidence / allegiance; (2) loss of advertiser confidence / allegiance; and, (3) loss of investor confidence / allegiance as a result of trends (1) & (2).

That first threat or trend was discussed in installments #1 and #2 of my ongoing “Media Metrics” series. Those essays documented the explosion of choices in the media marketplace and showed how many consumers are opting for new media and technology options over older media outlets and options. Installment #3 in the series documented the seismic shifts underway in the advertising marketplace, with ad dollars rapidly flowing away traditional media operators and toward new media and technology providers. Here in installment #4, I will discuss how traditional media operators and new media / technology operators are trading places in terms of investor confidence.

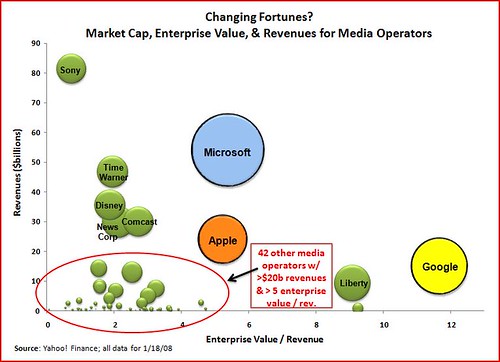

Exhibit 1

As the collective eyes and ears of consumers migrate to new media technologies and outlets, investors are increasingly diverting their dollars to new media operations, (that are largely unregulated) and abandoning traditional media operators (many of which remain heavily regulated). Exhibit 1 above provides a snapshot of the marketplace situation as of Jan. 18. The chart uses three financial metrics that Wall Street analysts commonly used to gauge the health of media operators: Enterprise value/revenue is plotted on the x axis. Revenues are plotted on the y axis. And the size of each company’s bubble on the chart is determined by its market capitalization.

This is not a pretty picture for traditional media operators. While some traditional media operators continue to attract a respectable level of investment and revenues, most are struggling to keep up with new players like Google, Apple and Microsoft. Importantly, as shown in the highlighted circle on the lower left of the chart, there are 42 major media operators that individually don’t have more than $20 billion in revenues (most have far less than that) and most of which also have market caps that look like rounding errors on a Microsoft or Google financial statement.

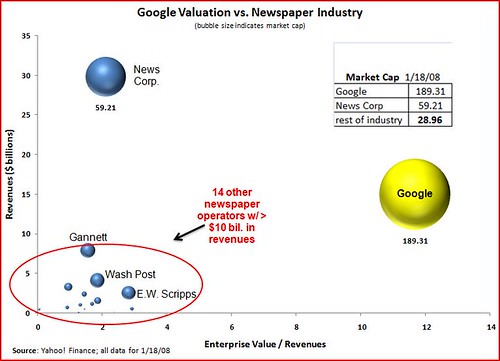

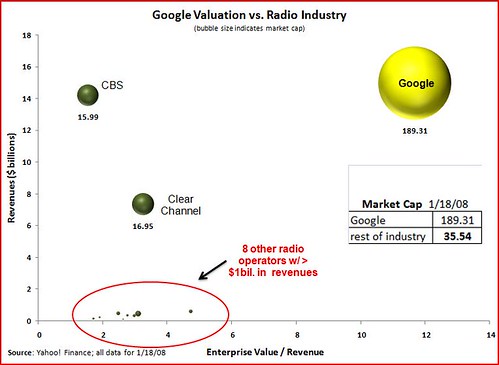

Let’s just compare just Google to two media sectors–newspapers and radio. Google is absolutely murdering these sectors right now by stealing away the attention of consumers and the allegiance of advertisers, so it’s a worthwhile comparison. As Exhibits 2 and 3 make clear, this situation is resulting in lost investor confidence in traditional media operators.

Exhibit 2

Exhibit 3

For newspapers, 14 of the leading providers in the U.S.–including The New York Times Co., The Washington Post Co., Gannett, Belo, and McClatchy–have a combined market cap of roughly $29bil, which is just 15% of Google’s whopping $189bil market cap as of January 18. Only a few of those traditional newspaper operators cross the $1billion threshold, and the largest, Gannett, has revenues of $7.8 billion, roughly half of what Google is pulling in. If you add News Corp. to the total (since they own the Wall Street Journal and New York Post) it helps bring the newspaper sector totals up a bit since Rupert Murdoch’s company has a $60bil market cap. (But much of that value is derived from other properties in his media stable including a TV network, broadcast stations, cable channels, satellite operations, and MySpace.com. Thus, it’s probably not fair to include a diversified company like News Corp. in the newspaper grouping.)

The situation for broadcast radio operators is equally bleak. The industry’s 10 leading providers have a combined market cap of $36bil., just 19% of Google’s. But, as will be shown in an upcoming installment in my Media Metrics series, broadcast radio operators are losing listeners and advertisers at an alarming rate. The broadcast radio sector is on the brink or a veritable doomsday scenario with satellite radio, non-commercial radio, iPods, digital downloads, Internet radio, cell phones, and other audio information and entertainment options eating away at their marketplace hegemony. In fact, satellite radio operators XM and Sirius have higher market caps than every radio broadcaster except for Clear Channel and CBS. And XM and Sirius can’t even turn a profit! So, traditional radio broadcasters are in real trouble.

OK, let’s wrap up by trying to answer the question that reporter asked me last year: Exactly how many old media companies would you need to stack on top of one another to equal the value of just Google? Answer: Quite a few!

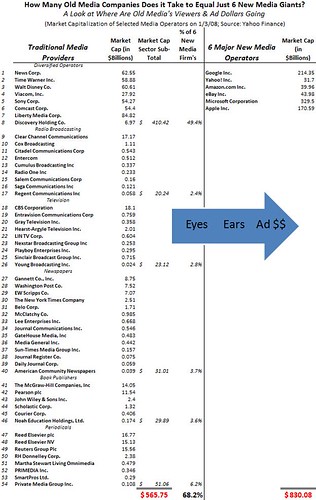

Actually, I decided to take a different cut at the question and grouped together 6 major new media / technology operators: Google, Microsoft, Apple, Yahoo!, Amazon.com, and eBay. I totaled their market caps on January 2 of this year and arrived at $830 billion. That’s a stunning number, and old media operators simply cannot come close to equally it today. As Exhibit 4 shows, I added up the market caps of 54 of the leading traditional media operations in America to compare them to those big 6 new tech companies. Amazingly, those 54 old media companies only got 70% of the way there at just $565 billion. Stated differently to add emphasis, as of the first week of January, just 6 major new media operators (Google, Microsoft, Yahoo, eBay, Amazon, and Apple) had a collective market capitalization that was 30% higher than the aggregate market cap of 54 of the most venerable names in traditional media.

Exhibit 4

[

Larger image available by clicking on image.]

[

Larger image available by clicking on image.]

This is a stunning change of fortunes. To summarize: Traditional media operators are struggling in the face of new competitive threats from within and without their sectors. They have been hemorrhaging consumers and ad dollars. And as all those eyes, ears and ad dollars migrate to new technology operators and media platforms, investors are following—in BIG numbers. That means less market confidence and less market capital for traditional media.

And what makes this situation even more insulting for many of these providers is that, as stated previously, they have their hands tied by regulation and are unable to respond to these competitive threats to stop the bleeding. Various ownership restrictions, market limitations, speech controls, and other meddlesome rules, encumber the ability of traditional operators to structure their business affairs as they wish to respond to the new threats. The result: An even greater loss of investor confidence. Why invest your money in a traditional media operator that is shackled with regulatory constraints when the new kids on the block of have all the cool toys and can use them however they wish?

The ramifications of these developments are profound for another reason. These “new media operators” I have been referring to aren’t really media operators in the traditional sense of the word at all. Or, to be more specific, they are not media creators; they are really just media aggregators and distributors. As digital visionary Jaron Lanier has noted:

“In the new [media] environment, Google News is for the moment better funded and enjoys a more secure future than most of the rather small number of fine reporters around the world who ultimately create most of its content. The aggregator is richer than the aggregated.”

I’ll leave it for another day and another blog post to discuss the ramifications of that fact. But it is a fact: The aggregators are now richer than the aggregated. To remedy this situation, we don’t need to resort to draconian solutions along the line of what neo-Luddites like Andrew Keen might suggest. We just need to make sure that all media operators are on a level playing field and have the ability to respond to competitive threats in America’s dynamic modern media marketplace.

[ Up next… Upcoming installments of the Media Metrics series will take a closer look at competition and choice in audio and video markets.]

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.

The Technology Liberation Front is the tech policy blog dedicated to keeping politicians' hands off the 'net and everything else related to technology.